Goldman Sachs has always been more aggressive in its technical explorations. It is rich in exploration and practice in this area. Recently, John Mahoney, vice president of Goldman Sachs Global Investment Banking, shared a number of industry observations and forecasts at a financial technology summit, some of which may be of particular interest to domestic readers.

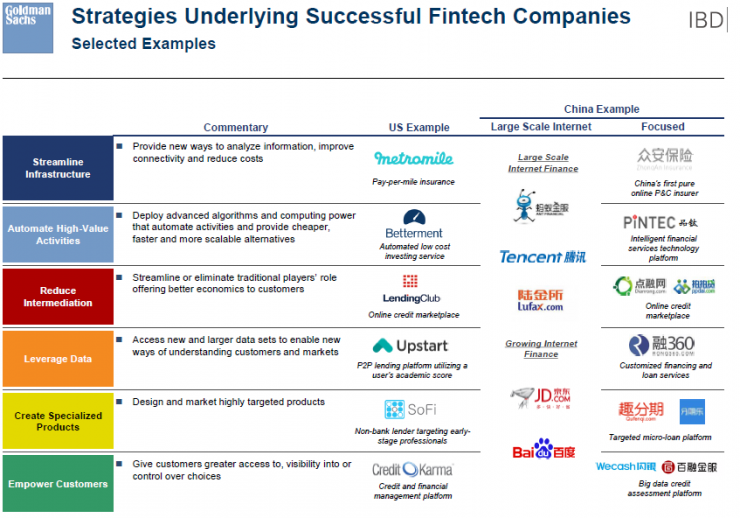

From this slide we can see that John Mahoney divided the financial technology companies with potential for success into 6 categories, each with simple comments and the corresponding case of China and the United States.

The first category is the process streamlining class, which provides a new method of data analysis to increase user stickiness while reducing costs. The representative company of the United States is Metromile, an auto insurance agency established in San Francisco in the United States in 2011. It changed the practice of fixed insurance for traditional automobile insurance and collected premiums according to the actual milestone; the domestic company is Zhong An Insurance. In the case of John Mahoney, it is “China. The first pure property insurance online."

The second category is high value-added business automation, which uses advanced algorithms and computing power to provide customers with cheaper and more efficient (financial investment) options. The United States has a well-known Betterment, domestic PINTEC, PINTEC is a subsidiary of the intelligent financial services group has a countdown, a little fund, building blocks box, Qilehui and other subsidiaries.

The third category is to go to the intermediary category, changing or streamlining the traditional business chain, the United States has LendingClub, China is a bit of financial and pat network, such companies mainly P2P lending, currently belongs to the focus of regulatory areas.

The fourth category is data efficiency, with a larger amount of data to serve the longer-tailed customers and niche markets, mainly digital credit and related retail banking. U.S. has Upstart, and China has 360.

The fifth category is highly customized financial products that can be applied to specific situations. For example, SoFis in the United States and China’s interesting stages and staged music are targeted at university student groups. These groups have lower ratings in traditional banks, but there are Certain loan demand and repayment ability.

The sixth category is wealth management tools that provide consumers with some data tools or services for investment decision making. The United States has Credit Karma, China has Wecash and Bairong gold clothes, these types of relatively more professional, higher audience threshold, so the visibility is not as good as the previous categories.

The sharing also mentioned that large Internet companies such as Ant Financial, Tencent, Lukin, Baidu, and Jingdong have all made financial attempts. They are less “special†and generally cross-border. As far as we know, these companies have already had some significant production values ​​in terms of practical effects.

The sharing of John Mahoney basically covered the mainstream financial technology industry, and also commented on their own unique skills. Process streamlining, automation of high-value-added services, deintermediation, data efficiency, and high customization are actually the development trend of the entire financial industry. The future financial technology companies will mainly focus on solving these problems. These “predecessors†are The road to struggle may give some lessons.

Headphone Cover,Earbuds Cover,Earphone Cover,Headset Covers

Nantong Boxin Electronic Technology Co., Ltd. , https://www.bosencontrols.com