Mentioned Monte Carlo (also translated as "Monte Carlo"), people can not help but think of the casino in Monaco. Is there a necessary connection between the two? The answer is: Exactly!

Think about it, what is gambling related to? The first thing that comes to mind is randomness and probability. Yes, the Monte Carlo method is related to probability theory and mathematical statistics.

MCM proposes:

The Monte Carlo method MCM was first proposed by members of the "Manhattan Project" project in the United States during the Second World War in the 1940s, SM Ulam and J. von Neumann (father of computers). The mathematician von Neumann named this method with the world-famous casino, Monaco's MonteCarlo, which cast a mysterious color on it. Prior to this, the Monte Carlo method already existed. In 1777, the French mathematician Georges Louis Leclere de Buffon proposed a method of needle injection to find the pi. This is considered to be the origin of the Monte Carlo method.

The traditional empirical method is difficult to obtain satisfactory results because it cannot approach the real physical process. Because the Monte Carlo method MCM can realistically simulate the actual physical process, the solution to the problem is very consistent with the actual situation, and a very satisfactory result can be obtained. This is also a calculation method based on the theory of probability theory and mathematical statistics. It is a method of solving many computational problems by using random numbers (or more common pseudo-random numbers). The solved problem is linked to a fixed probability model, and an electronic computer is used to implement statistical simulation or sampling to obtain an approximate solution to the problem. To symbolically indicate the probabilistic and statistical characteristics of this method, the casino-Monte Carlo name was borrowed. This naming not only reflects part of the connotation of the method, but also is easy to remember, so it is generally accepted by people.

BTW: The word MonteCarlo comes from Italian to commemorate Prince Charles III of Monaco. Although Monte Carlo is a casino, it is small and is estimated to be about the same size as a street in Beijing.

MCM overview:

The Monte Carlo Method (MCM), also known as random sampling or statistical simulation, was proposed in the mid-1940s due to the development of science and technology and the invention of electronic computers. A very important numerical calculation method that guides. Refers to the use of random numbers (or pseudo-random numbers) to solve many computational problems. Corresponding to it is a deterministic algorithm. Monte Carlo methods are widely used in financial engineering, macroeconomics, computational physics (such as particle transport calculations, quantum thermodynamics calculations, aerodynamic calculations) and machine learning in artificial intelligence .

The basic idea of ​​MCM:

When the problem solved is the probability of occurrence of a random event, or the expected value of a random variable, the probability of the random event is estimated by the frequency of occurrence of such event by some "experimental" method, or the randomness is obtained. Some numerical characteristics of the variable and use it as a solution to the problem.

There are a class of problems whose dimensions (number of variables) may be as high as hundreds or even thousands. The difficulty of solving problems increases exponentially with the increase of the number of dimensions. This is the so-called "Curse of Dimensionality". Even with the fastest computers, traditional numerical methods are difficult to deal with, but the computational complexity of the Monte Carlo method MCM is no longer dependent on the dimension, and MCM can be used to deal with dimensional disasters. To improve the efficiency of the method, scientists have proposed many so-called "variance reduction" techniques.

Another type of method similar to the Monte Carlo method MCM, but the different theoretical basis - "Quasi-Monte Carlo method" (Quasi-Monte Carlo method) - has also developed rapidly in recent years. The "Hua-King" method proposed by Chinese mathematicians Hua Luogeng and Wang Yuan is one of them. The basic idea of ​​this method is to replace the random number sequence in the Monte Carlo method MCM with deterministic Low Discrepancy Sequences. This method solves some problems more than the Monte Carlo method MCM. Hundreds of times, the calculation accuracy has also been greatly improved.

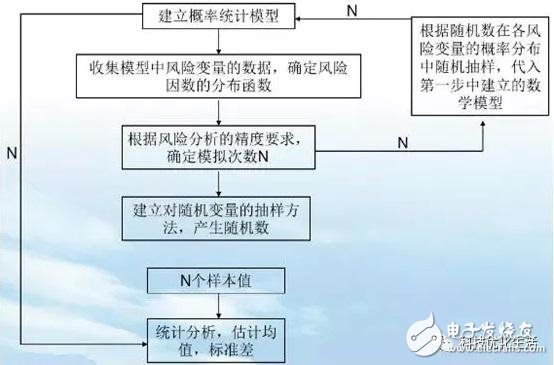

The basic principle of MCM

It is known from the probability that the probability of an event can be estimated by the frequency of occurrence of the event in a large number of trials. When the sample size is large enough, the frequency of occurrence of the event can be considered as its probability. Therefore, a large number of random samples are randomly selected for the random variables that affect their reliability, and then these sample values ​​are substituted into a functional function group to determine whether the structure is invalid, and finally the failure probability of the structure is obtained. MCM is based on this idea for analysis.

There are statistically independent random variables Xi(i=1,2,3,...,k) whose corresponding probability density functions are fx1, fx2,...,fxk, and the functional function is Z=g(x1,x2, ..., xk).

First, according to the corresponding distribution of each random variable, N sets of random numbers x1, x2, ..., xk values ​​are generated, and the function function value Zi = g (x1, x2, ..., xk) is calculated (i = 1, 2, ..., N) If there is a functional function value Zi ≤ 0 corresponding to the L group random number, then when N→∞, according to Bernoulli's large number theorem and the characteristics of normal random variables are: structural failure probability, reliable index.

From the idea of ​​MCM, it can be seen that MCM can avoid the mathematical difficulty in structural reliability analysis. Regardless of whether the state function is nonlinear or not, whether the random variable is non-normal, as long as the number of simulations is sufficient, a more accurate failure probability can be obtained. And reliability indicators. Especially when the coefficient of variation is large, the result is more accurate than the reliable index calculated by the JC method, and it is easy to program because of the simple idea.

MCM main steps:

The Monte Carlo method of work can be summarized into three main steps:

1) Construct or describe a probability process

For the problem of random nature, it is mainly to correctly describe and simulate this probabilistic process. For a certainty problem that is not a random nature, an artificial probability process must be constructed in advance. Some parameters of it are exactly the solution to the required problem. . Problems that are not random in nature are translated into problems of random nature. If you have an inappropriate analogy, you have difficulties in your work and you have to face difficulties. If you have no difficulties, you must create difficulties and meet difficulties. ^_^

2) Implement sampling from known probability distributions

After the probabilistic model is constructed, since various probabilistic models can be regarded as composed of various probability distributions, a random variable (or random vector) with a known probability distribution is generated, which is a Monte Carlo simulation. The basic means of experimentation, which is why the Monte Carlo method is called random sampling. A random number is a random variable with a probability distribution. Random numbers are the basic tool for implementing Monte Carlo simulations. A random number sequence is a simple subsample of a population with such a distribution, that is, a sequence of independent random variables with such a distribution. The problem of generating random numbers is the sampling problem from this distribution. On a computer, random numbers can be generated physically, but they are expensive, cannot be repeated, and are inconvenient to use. Another method is to generate it using a mathematical recursion formula. The sequence thus generated is different from the true random number sequence, so it is called a pseudo random number (or a pseudo random number sequence). However, after various statistical tests, the pseudo-random number (or pseudo-random number sequence) has similar properties to the real random number (or random number sequence), so it can be used as a true random number.

3) Establish various estimators

After the probability model is constructed and can be sampled from it, after the simulation experiment is realized, a random variable is determined as the solution to the required problem, which is called unbiased estimation. Establishing various estimators is equivalent to examining and registering the results of the simulation experiments, and obtaining solutions to the problems.

The Monte Carlo method usually solves various practical problems by constructing random numbers that conform to certain rules. For those problems that are too complicated to calculate to solve the solution or have no analytical solution at all, the Monte Carlo method is an effective way to find the numerical solution.

MCM work process:

There are two main parts to applying the Monte Carlo method when solving practical problems:

1. When Monte Carlo method is used to simulate a process, it is necessary to generate a random variable with a certain probability distribution.

2. Estimate the digital features of the model by statistical methods to obtain a numerical solution to the actual problem.

In theory, the Monte Carlo method requires a lot of experimentation. However, the approximate solution is obtained. The larger the number of simulated samples, the more experiments, and the more accurate the results are. However, an increase in the number of samples will lead to a significant increase in the amount of calculation.

MCM estimates the pi:

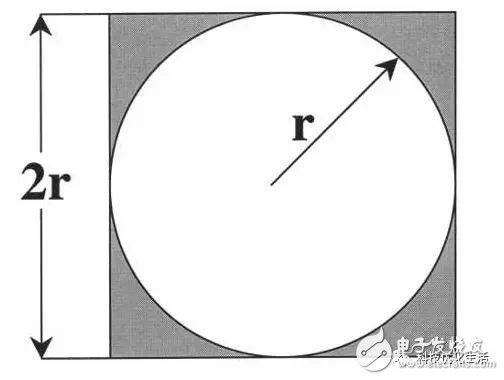

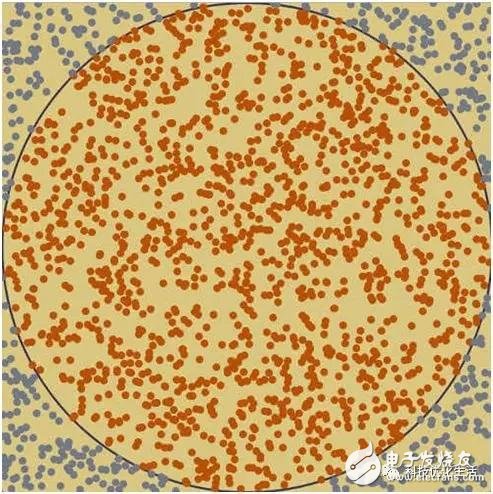

Using the Monte Carlo method, as shown in the figure, a circle of radius r is made in a square with a side length of 2r. The area of ​​the square is equal to 2r & TImes; 2r = 4r^2, the area of ​​the circle is equal to π & TImes; r & TImes; r = πr ^2, from which it can be concluded that the ratio of the area of ​​the square to the area of ​​the circle is 4: π. Suppose that a dart is randomly thrown onto a square target. If the hit point is evenly distributed on the target, that is, the coordinates of a point are scattered in the square, then the number of points N falling within the square and falling within the circle The ratio of the point K is close to the ratio of the area of ​​the square to the area of ​​the circle, that is, N: K ≈ 4: π, and therefore, π ≈ 4K/N . Using this method to find the pi, you need a large number of evenly distributed random numbers to get a more accurate value.

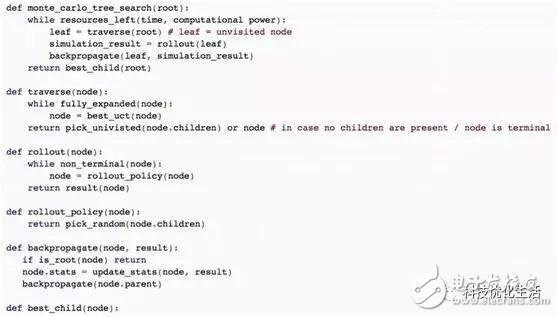

MCM evaluates the Go board:

We all know Google's DeepMind Go program AlphaGo and its powerful computing power beyond humans. In fact, the Monte Carlo method of thinking is also used in the evaluation of the board. Each Go board has an "optimal value", which corresponds to the final result of the Go board obtained by both sides of the game using the perfect move. It has been proved for Go that the time to calculate this "optimal value" increases exponentially at least with the number of steps between the face and the end of the game. For example, if the average step is 200 steps, the average number of steps per step is increased by 200 times. Theoretically, the "optimal value" cannot be obtained, so people think of using the Monte Carlo method to sample some of the entire possibility space, and then approach the "optimal value" by statistical estimation. This is a dynamic evaluation method called Monte Carlo tree search proposed in 2006.

Although the existing Monte Carlo tree search can ensure that the results of a large number of samples are enough to converge to the "optimal value" of the disk surface, the number of samples required to achieve "sufficient convergence" is still exponentially increasing with the size of the entire possibility space. However, in the practice of the chess game, the Monte Carlo tree search does show far more than the traditional method in the case of limited game time. In recent years, people have added more expert knowledge related to Go in the selection strategy, which makes the level of the chess game system based on Monte Carlo tree search continuously improved. Monte Carlo tree search has become a key technology for making decisions in a perfect information game scenario, and has broad prospects in many real-world applications.

MCM application areas:

More and more extensive. It not only solves the difficult and complex mathematical calculation problems such as multiple integral calculation, differential equation solving, integral equation solving, eigenvalue calculation and nonlinear equations solving, but also in statistical physics, particle transport calculation, quantum thermodynamics. A wide range of fields such as computation, aerodynamics, nuclear physics, vacuum technology, systems science, information science, utilities, geology, financial engineering, macroeconomics, biomedicine, reliability, computer science, and machine learning for artificial intelligence Have been successfully applied.

MCM development history:

1) In the early 20th century, although the number of experiments was thousands, the pi value obtained by Monte Carlo method could not reach the estimation accuracy of Zu Chongzhi in the 5th century. This may be the main reason why the traditional Monte Carlo method has not been promoted for a long time.

2) The development of computer technology has made the Monte Carlo method popularized in the last 10 years. The modern Monte Carlo method has not had to do experiments by hand, but with the high-speed operation of the computer, the original time-consuming and laborious experiment process has become a quick and easy task. It is used not only to solve many complex scientific problems, but also to be used frequently by project managers.

MCM advantages:

1) The algorithm is simple, eliminating the complicated mathematical derivation and calculation process, so that the average person can understand and master;

2) The adaptability is strong, and the complexity of the geometric shape of the problem has little effect on it;

3) The speed is fast, the convergence of the method refers to convergence in the sense of probability, so the increase of the problem dimension does not affect its convergence speed;

4) Storage is small, and the storage unit when dealing with large and complex problems is very economical.

MCM disadvantages:

If the input of a random number in a pattern is not a random number as envisioned, but constitutes a subtle non-random pattern, then the Monte Carlo method of solving the problem may be wrong.

MCM compared with GA:

Monte Carlo method MCM and genetic algorithm GA (please participate in the public number "scientific optimization life" - artificial intelligence (28)) and other intelligent optimization algorithms have similarities, are all random approximation methods, can not guarantee the optimal solution, etc. But they also have essential differences. 1) Different levels, MCM can only be called method, GA is a bionic intelligent algorithm, much more complicated than MCM. 2) Different application fields, MCM is a kind of simulation statistical method. If the problem can be described as a form of statistic, then it can be solved by MCM; while GA is suitable for large-scale combinatorial optimization problems, as well as complex functions. Find the best value, parameter optimization, and so on.

Conclusion:

The Monte Carlo method MCM, also called statistical simulation method, is a very important numerical calculation method guided by probability and statistics theory. Refers to the use of random numbers (or more common pseudo-random numbers) to solve many computational problems. The Monte Carlo method MCM solves various practical problems by constructing random numbers that conform to certain rules. It is widely used in financial engineering, macroeconomics, computational physics (such as particle transport calculation, quantum thermodynamics calculation, aerodynamic calculation) and artificial intelligence machine learning.

5G Cpe,Wifi 6 Router,5G Wifi Router,5G Sim Card Router

Shenzhen MovingComm Technology Co., Ltd. , https://www.movingcommtech.com