After experiencing the double pressure of market downturn and sharp rise in raw material prices, the refrigerator market seems to be turning around with the market warming up and the continuous optimization of product structure. Although the sales trend is still not shocking, the sales volume is still good. . At the 2018 China Refrigeration Industry Summit Forum held recently, Wang Lei, vice chairman of the China Household Electrical Appliances Association, said that in recent years, the refrigerator industry as a whole is still in a sideways position, and industry competition has reached the final stage. So in this key link of comprehensive strength, "research and development capabilities, innovation capabilities, marketing capabilities, supply chain integration capabilities are indispensable", those small and medium-sized refrigerator companies under the pressure of the first-line brands have a good time?

Raw materials are rising step by step

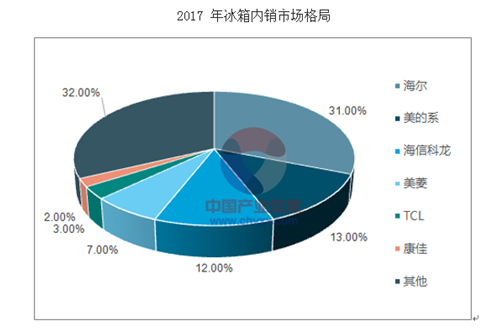

The refrigerator market since 2017 has been highly polarized. The prices of upstream raw materials such as black materials have risen step by step, and mainstream refrigerator enterprises rely on large-scale procurement capabilities to have the bargaining power of leading upstream suppliers. On the basis of raising the average price, it has generally shown a good momentum of steady growth, and even with the opportunity of rising raw materials, it has continuously squeezed the living space of SMEs. According to the data, the domestic market share of the refrigerator market in 2017 was Haier (30.9%), Midea (12.5%), Hisense Kelon (12.4%) and Meiling (6.8%), and CR4 increased by 4.1pct in 2016. To 62.7%. In 2017, the raw material price increase cycle actually benefited the mainstream companies to share their shares, and the refrigerator industry brand concentration was getting higher and higher.

In contrast, the price of raw materials is pressing harder, making small and medium-sized refrigerator companies start to struggle on the cost of life and death. From the relevant annual reports or announcement data, they can pry into their miserable market conditions.

Oma Electric (002668) disclosed the 2017 annual report on the evening of April 19, the company's annual operating income was 6.964 billion yuan, an increase of 38.14%; the net profit attributable to shareholders of listed companies was 381 million yuan, an increase of 25.15%. Under the background of the increase in revenue and profits, the refrigerator business “sales reached 8,884,700 units, an increase of 20% year-on-year; the revenue of 6.241 billion yuan, a 32% year-on-year increase.†The data looks like brilliance, but “the gross profit margin is reduced by 8 Percentage points, net profit is also 6% lower than last year, but it has exposed its impact on exchange rate fluctuations and raw material price increases.

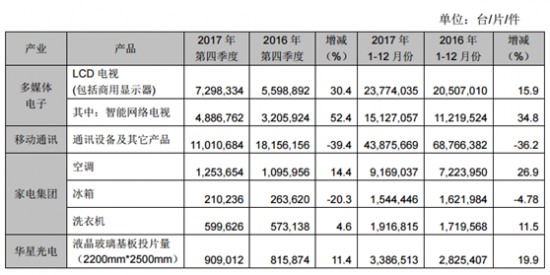

TCL Group's 2017 annual report did not specifically mention the specific sales volume of the refrigerator and the revenue and profit data. Only the company's product structure continued to be optimized, and the proportion of high-end products such as inverter air conditioners, air-cooled refrigerators and pollution-free washing machines increased steadily. Business data is ambiguously taken. However, in the announcement of the product sales and service business in the fourth quarter of 2017 released in early January, it can be seen that in the home appliance industry, the sales volume of TCL's air conditioners and washing machine products increased by 26.9% and 11.5% respectively, but the refrigerator. Sales volume has not unexpectedly declined. The data in the table below clearly shows that in 2017, TCL refrigerators sold 1.54 million refrigerators, down 4.78% year-on-year.

“The price of raw materials is rising, and the ability of big brands to absorb and absorb is stronger.†In a recent survey conducted by China National Grid, a person in charge of a small and medium-sized refrigerator company told reporters that “the lack of scale has become our current disadvantage.â€

From the previous "four golden flowers" to the current "1+4+N", the speed of brand concentration in the refrigerator industry has continued, and the increase in raw materials has accelerated this process. The monitoring data of the Ovi cloud network shows that 2017 In the first quarter of the year, the market share of the TOP5 brand of refrigerators was 72.6%. By the first quarter of 2018, the market share of TOP5 brands had reached 77.6%. At this time, the market space left for many small and medium-sized enterprises is only 20%, and the increasingly obvious trend of giant competition will only speed up the elimination of small and medium-sized brands.

The big brand channel sinks down on the line and the third and fourth line markets are squeezed

According to the omni-channel data of Ovi Cloud, the retail volume of refrigerators in the country was 33.76 million units in 2017, of which the online market retail volume was 12.23 million units; the retail volume of the Chinese refrigerator market in January-April 2018 was 9.2 million units, including The online market retail volume was 3.35 million units. From the data since 2017, online market sales accounted for 36% of the overall market share, and still maintain rapid growth in the overall stable market of the domestic refrigerator market. In the survey conducted by China National Grid, it was found that the online market of most SMEs has been in a state of loss. Even some enterprises have reduced their online channel investment due to unsatisfactory online conditions, and discarded 36% of the market space. In the face of continued growth in market opportunities, we will devote all our energy to the third- and fourth-tier markets that have always been proud of ourselves and that we still have advantages. But is the advantage really an advantage?

According to the monitoring data of Ovi Cloud, the retail sales of Guangxi, Henan, Jiangxi, Ningxia, Shanxi and Xinjiang increased respectively compared with the year-on-year growth of 2.1% in the first to third grades of the country from January to April 2018. 10.8%, 6.2%, 12.1%, 10.5%, 7.0%, 14.9%. In the case of the country's township market retail sales increased by 5.8% year-on-year, the retail sales of Fujian, Guangxi, Guizhou, Hunan, Jiangxi, Inner Mongolia, Ningxia, Shandong, Shaanxi, and Tianjin townships increased by 17.6%, 9.1%, 16.0%, and 9.6, respectively. %, 24.2%, 16.6%, 51.3%, 10.6%, 12.9%, 11.8%. According to the information released by Jingdong Household Appliances, from the market-level sales situation, the proportion of sales in the fourth, fifth and sixth grades continued to rise, and sales maintained a relatively high growth rate.

The above data shows that the third- and fourth-tier markets still have great development potential, but this potential is not only seen by SMEs who have entered the market first. With the rise of new retail, whether it is the pure electricity business represented by Jingdong Ali, or Suning Gome, which has obvious advantages under the line, has accelerated the penetration into the offline. E-commerce companies and traditional offline enterprises jointly explore new retail models, which also indicates that online and offline are deep integration, multi-channel marketing is gradually taking shape, and multi-channel marketing is compared to small and medium-sized enterprises that are mainly in the low-end market. The advantages of high-end brand awareness, strong product reliability, and mainstream refrigerator companies with both online payment and offline experience are self-evident.

In addition to the layout of new retail enterprises such as Jingdong Ali Suning Gome, the mainstream refrigerator companies have also accelerated the layout of the third and fourth line markets, and have begun to establish specialty stores. "Only focusing on the first- and second-tier markets, big brands began to exert their strength in the third- and fourth-tier markets. Our promotion capabilities and other aspects were not as strong as before." A small and medium-sized enterprise told China National Grid when interviewed. The integration of online and offline channels has become a new trend, and the big brands deep-rooted in the third- and fourth-line markets are bound to further squeeze the survival space of small and medium-sized brands.

Difficulties in recruiting workers and brain drain

The external environment is in crisis and the internal hidden dangers have never stopped. In the recent survey of China National Grid, most refrigerator companies, especially small and medium-sized refrigerator companies, generally reflect a problem – recruitment is difficult.

According to the China National Grid Survey, the difficulty of recruiting workers is a major problem facing the entire industry. However, this is particularly evident in the SMEs. "It is difficult to recruit workers, difficult to work, and difficult to keep people." "Temporary workers are looking for a good job, and long-term work is hard to find." This is the status quo of a small and medium-sized refrigerator company to reporters. As the market becomes more diversified, the employment channels of young people are beginning to diversify, which makes enterprises, especially manufacturing, face enormous challenges due to their high level of hard work.

According to the person in charge of the company, the company is currently facing two major pressures: the first is the efficiency and quality pressure, the current market situation is difficult to take into account both quality and efficiency; the second is the safety pressure, the new employee mobility, due to operation Unskilled people will have potential safety hazards, and the occurrence of safety accidents will not be accountable to the employees themselves and the company itself.

Another small and medium-sized enterprise reported that the shortage of personnel directly led to a serious shortage of refrigerator capacity. "The company's current production line is there, there is no one, and there are always hundreds of people missing for a long time, and two production lines are vacant without a few hundred people." The person in charge of the company even said "if the personnel are satisfied, maybe this year's Total sales will increase by 20%-30%.".

In addition to the difficulty of recruiting workers, brain drain is also a major worry for these SMEs. Most of the SMEs who visited the survey said that the loss of a large number of R&D personnel and even the R&D team directly led to a longer development cycle of refrigerator products, further losing the opportunity to occupy the market.

It is difficult to break the gap under the pressure of industry shuffling

After nearly 40 years of rapid development, China's refrigerator industry has gradually entered the "second half", production and sales scale will be stable, Lu Shenghua, editor-in-chief of China National Grid, believes that upgrading and structural upgrading has become the main theme of industry development.

Internal and external troubles, the almost stagnant refrigerator market has brought unprecedented pressure to SMEs, how to break the bureau has become a top priority, and the differentiation strategy has been quickly put on the agenda.

During the survey, China National Grid also saw some small and medium-sized refrigerator enterprises that have outstanding performance on differentiated products: the unique stainless steel inner tank refrigerator products with high processing precision have won certain recognition in the market. Liu Shikun, deputy general manager of the Premier Electric Group, is quite confident in his stainless steel products. He threatened that the company's goal this year is to make more than 100,000 units. On the other hand, due to the optimistic view of the embedded refrigerator market, it has also established a distinguished product line that continues to adhere to differentiated product lines and focuses on embedded products.

Jinghong Refrigerator has always adhered to the high-end route, and made a certain breakthrough in the small and medium-sized exquisite refrigerator products. He Xuebin, general manager of Jinghong Electric, believes that as the population ages, the retired workers have more leisure time and energy. In the vegetable market or supermarket, fresh fruits and vegetables are purchased, and there is no need to store too much food in the refrigerator. At this time, small and medium-sized refrigerators will usher in new market demand, so he said that “Jinghong has exerted strength in addition to fresh-keeping technology and embedded smart home. It will also continue to invest in the research and development of sophisticated, small and medium-sized refrigerator products."

However, the status quo is: in the face of stagnant markets, while small and medium-sized brands are exerting force, mainstream refrigerator companies have also launched their own differentiated products to seize the market. Such as Haier full space fresh-keeping refrigerator, "micro-crystal fresh" refrigerator, Meiling "M fresh series refrigerator", equipped with all-ecological sterilization technology and full-time super-quiet technology Rongsheng refrigerator, Hisense boutique "Tianlu series more open doors Refrigerator" and so on. In the case that the demand in the refrigerator market is not strong and the demand for segmentation is accelerating, the big brands are more capable of building their own differentiated products, and at the same time more capable of optimizing and upgrading the products. In contrast, the so-called “advantages†of SMEs. I was suppressed again.

As Guo Meide, vice president of Aowei Cloud Network, said, in the case of comprehensive cost continuous pressure and cross-border brands rushing to eat cakes, the scale advantage of mainstream refrigerator enterprises and the competitive advantage of high-end market are prominent, and the survival status of small and medium-sized brands is worrying and facing The danger of shuffling out. (Jia Qiong)

DIP Power Inductor is a small choke coil power inductor. It has a wire wound on the core(magnetic or air), with leads attached to it for through-hole mounting. The feathure is Low DC resistance, high current handling capacities, wide range of inductance which is best for the power supply line. It widly used for noise filter, motor controller and switching power supply,LED lights, Adapters,Electrical ballasts,DC-DC converters, TVs, VTRs, personal electronics, home appliances, ect.

An inductor is a passive electronic component which is capable of storing electrical energy in the form of magnetic energy. Basically, it uses a conductor that is wound into a coil, and when electricity flows into the coil from the left to the right, this will generate a magnetic field in the clockwise direction.

|

Ferrie Drum Core inductor |

|

|

Components : Ferrite core, Copper wire;Tube,Lead wire Core : Ferrite core-NiZn Wire : Enameled copper wire-UEW/PEW Tube : UL heat-shrinkable tube/PVC Lead wire : Tinned copper wires Glue : Epoxy Resin |

|

|

Functions |

Energy Storage; Filtering; Voltage Step-up; Resonance |

|

Coil Structure |

Drum type; Tubby type |

|

Characteristics |

Working Frequency Range Above 1KHZ Inductance Range 1uH-1H DCR Range unknown-Depend on customers' request Storage Temperature -20℃ to +85℃ Working Temperature -20℃ to +105℃ Storage Humidity 30% to 95% Available in E12 Series Small diameter of only 5.8 mm maximum Profile of 4.8 mm |

|

Test Items

|

Turns Ratio Inductance DC resistance test Safety test Current test |

|

Applications |

1. Digital Products:Digital camera ETC

2.Household Appliance:washing machine,air condition,air purifier,coffee maker, bread maker ETC 3. Security products:Camera,Voice recording equipment,memory device,infrared devices,alarms ETC 4.Switching power supplies for portable communication equipment, LCD TVs, car radios, camcorder, UPS ETC 5.Lighting industrial: LED drivers 6.Auto electronics: Navigator,Data recorder, Car charger ETC 7.Toys:electric toys, remote controller ETC 8.Motors 9 Input / output of DC/DC converters |

Dip Type Inductor,Custom Power Inductor,Power Choke Inductor,Ferrite Core Power Inductor

Shaanxi Magason-tech Electronics Co.,Ltd , https://www.magason-tech.com